The Lithium Briefing: Why the Smartest Money in Zimbabwe Will Be Lithium Money Within 36 Months

Whatever you are worth today, lithium is about to multiply the economy you are worth it in.

Take what you own. Your property, your business, your holdings. Now consider this: Zimbabwe's entire mining sector currently generates about 7 billion dollars a year. Lithium contributed roughly 500 million of that in 2025. If the beneficiation strategy that Treasury has quietly engineered reaches even its first stage of chemical processing, lithium alone will generate 2 to 3 billion dollars annually by 2028. If stage two arrives, 4 to 5 billion. If Zimbabwe captures the cathode precursor step, 8 billion. At that point, lithium would exceed the current value of every other mineral Zimbabwe produces combined.

When a single commodity reshapes the revenue base of an entire economy, it reshapes everything denominated in that economy. Property values. Stock prices. Consumer demand. Government spending. The purchasing power of every dollar circulating inside the country. The question for anyone who considers themselves good at making money is not whether they believe in lithium. The question is whether they can afford to be late to it.

The rock itself is worth almost nothing. A tonne of raw spodumene ore at the mine gate sells for fifty dollars. Crush it, float it, concentrate it to 6 percent lithium oxide, and that tonne becomes 1,200 dollars. Roast the concentrate at a thousand degrees, add acid, purify, and the resulting lithium hydroxide commands 20,000 dollars per tonne. Mix it into cathode material and it reaches 22,000. Pack it into a battery cell and the value hits 90 dollars per kilowatt-hour. Assemble the pack that goes into an electric vehicle and you are at 108 dollars per kilowatt-hour.

The multiplication from ore to battery pack: seventy-two times.

Zimbabwe has been selling the fifty-dollar version. The chemistry happened in China. The cathode happened in China. The cells happened in China. The seventy-two times happened everywhere except here.

On February 25, Mines Minister Polite Kambamura banned all raw lithium and concentrate exports with immediate effect. The fiscal architecture beneath that ban, designed by Permanent Secretary George Guvamatanga and Minister Mthuli Ncube, is the most sophisticated mineral taxation system on the African continent. And the 1.4 billion dollars in Chinese processing investment already committed means this is not a plan. It is a structure with concrete being poured.

The Fiscal Machine That Nobody Is Talking About

The export ban gets the headlines. The fiscal gradient beneath it is where the genius lives.

The 2026 budget introduced a 10 percent export tax on lithium concentrate. On lithium sulphate, the first meaningful processed product, the tax is zero. VAT is zero. The spread between those two rates speaks to mining executives in the only language they read fluently, which is margins. Ship concentrate and you lose 10 percent off the top. Process it into sulphate on Zimbabwean soil and you keep everything.

Guvamatanga went further. The Quoted Price Method now values all mineral exports against international benchmarks, not the invoiced price between related parties. This closes the transfer pricing gap that bled revenue for years. Loss carry-forward deductions are capped at 30 percent. Capital write-offs are stretched across the life of the mine rather than front-loaded into the construction phase. For investors committing over 100 million dollars, corporate tax drops from 24.72 percent to 15 percent, customs duties are waived, and VAT on equipment is deferred.

At the February Mining Indaba, Guvamatanga presented this framework to a room where executives had just watched the DRC revoke permits and Ghana stall for two years on ratifying a single mining lease. He called Zimbabwe a safe haven for mining investment. The room was listening.

The budget allocated 789 million ZiG to the Ministry of Mines. It funded a nationwide Geomagnetic Airborne Survey to identify new deposits. It strengthened the Metallurgical Research Institute to assay outbound ores and plug leakage. The Mines and Minerals Bill is targeted for enactment this year.

This is not a single decision. It is a system of interlocking decisions designed by people who understand exactly how mining companies allocate capital.

The Geology and the Names That Matter

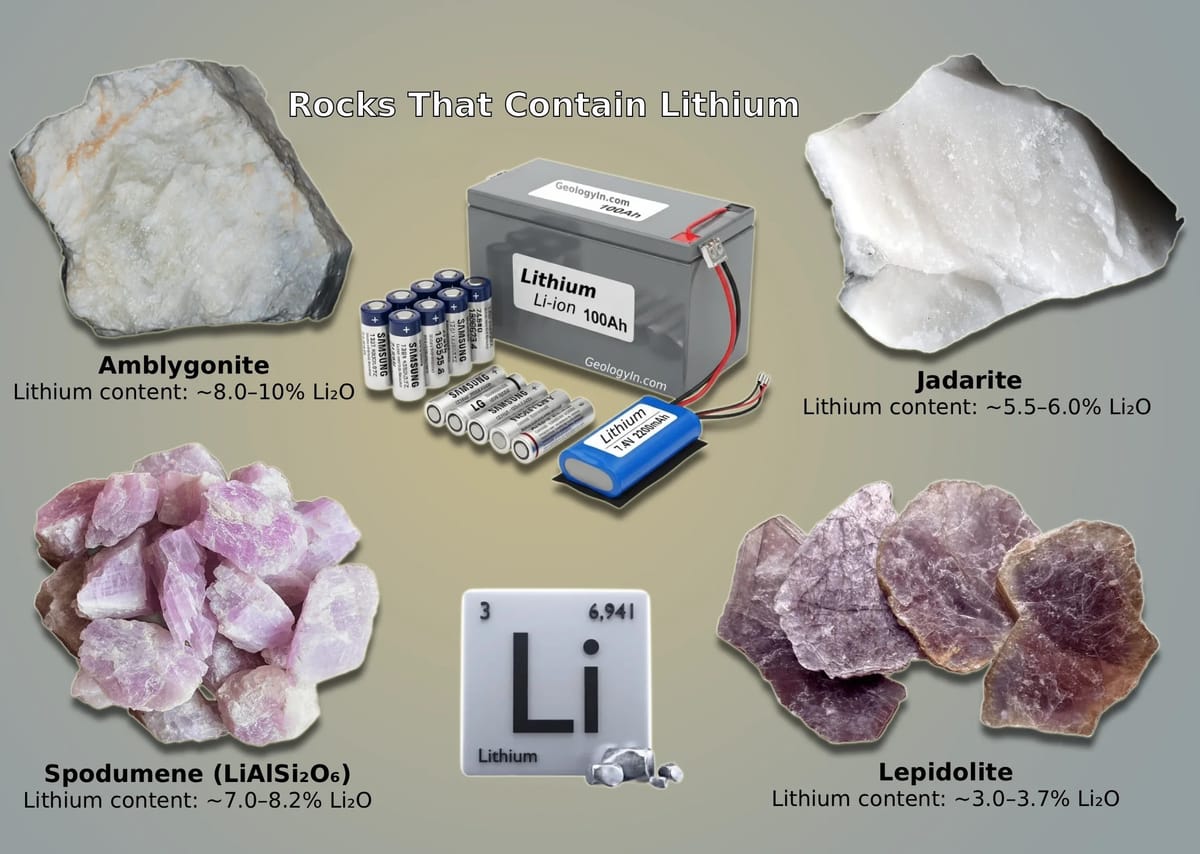

Zimbabwe holds Africa's largest lithium reserves. Five hundred thousand metric tonnes of contained lithium. Fourth-largest producer in the world. Ninety-seven percent of all lithium mined on the continent comes from Zimbabwean soil.

The deposits span a belt from Goromonzi through Mberengwa to Bikita. Arcadia runs at 1.19 percent lithium oxide, matching Australia's Pilgangoora. Bikita holds 54.5 million tonnes of ore resources. Sabi Star reaches 1.98 percent, approaching Greenbushes in Western Australia. And Sandawana in Mberengwa, the one most people have not heard of, has identified 600 million tonnes of pegmatite. It may be the largest single lithium-bearing structure in the country.

The Zimbabwean names on the levers matter as much as the geology.

President Mnangagwa personally commissioned both the Arcadia concentrator and the Sabi Star processing plant. These were not ceremonial. They were signals that the presidency sits atop the lithium value chain and intends to remain there.

John Mangudya, the former Reserve Bank Governor now heading the Mutapa Investment Fund, dismantled the old Kuvimba conglomerate model and reorganised it into five commodity-specific verticals. Mutapa Energy Minerals, under Innocent Rukweza, is now the state's direct operational vehicle in lithium. Production at Sandawana is forecast to increase fivefold this year. The 250-million-dollar concentrator being built through the Huayou-Tsingshan joint venture operates on a Build-Operate-Transfer model. Chinese capital builds it. Chinese engineers operate it. And within an agreed timeframe, the asset transfers to Zimbabwean state ownership.

Vice President Chiwenga has declared Sandawana will become Zimbabwe's premier industrial hub. Ncube designed the fiscal gradient. Guvamatanga presented the investment case to the world. Kambamura pulled the trigger on the ban. These are named individuals making specific decisions that are reshaping the economic geography of Southern Africa.

The 1.4 billion dollars in committed processing investment across six Chinese companies, Huayou at Arcadia and Sandawana, Sinomine at Bikita, Yahua at Kamativi, Chengxin at Sabi Star, Tsingshan at Gwanda, is not a memorandum of understanding. It is mines in production, concentrators commissioned, and chemical plants under construction. Huayou's 400-million-dollar lithium sulphate plant at Arcadia began commissioning in the first quarter of 2026. Yahua broke ground on its Kamativi sulphate facility on February 26, the day after the export ban, a timing coincidence that tells you the company had advance knowledge and was already moving.

The Insight That Changes the Conversation

Here is what separates this analysis from everything else you will read about Zimbabwean lithium.

The US Inflation Reduction Act's Foreign Entity of Concern provisions exclude lithium processed by Chinese companies from American clean energy tax credits. Every Western automaker is now desperately seeking non-Chinese lithium supply chains. Zimbabwe's geology qualifies. Its current Chinese-dominated ownership structure does not.

The country that offers Western-partnered lithium processing alongside its Chinese operations would unlock a dual-track supply chain serving both hemispheres. Chinese sulphate plants feeding the Asian EV market through one channel. A Western-partnered cathode facility qualifying for IRA incentives and serving North America and Europe through another. Both drawing from the same Zimbabwean ore. Both employing Zimbabwean workers. Both paying Zimbabwean taxes. Both giving Zimbabwe leverage over both sides of the great power competition.

Chile is already doing this through its Codelco-SQM joint venture. Australia does it through its Critical Minerals Strategy. Zimbabwe has the geology to play both sides. Guvamatanga's 20-million-dollar budget allocation for partnerships with investors willing to establish lithium battery manufacturing is the seed of this idea. It needs to become a tree.

Imagine a Special Economic Zone at Sandawana. Chinese processing on one side. A Western cathode facility on the other. Zimbabwe becomes not a supplier to one superpower but indispensable to both. That is not a ten-year vision. The geology, the fiscal architecture, and the geopolitical demand all exist today.

The One Honest Problem

Electricity.

Peak demand: 1,900 megawatts. Generation: approximately 1,200. Deficit: over 700. Kariba's southern station produces 185 megawatts of its 1,050 capacity. Lithium sulphate production requires 15 to 20 megawatts per facility running continuously. Chemical processing does not tolerate load-shedding. It does not pause. It fails.

The 400-million-dollar Afreximbank-funded solar project at Kariba, potentially 1,000 megawatts, would close most of this gap if it materialises. Captive solar at mine sites, which the Chinese operators have the capital to build, can bridge the rest. The electricity problem is solvable. But every month of delay costs an estimated 5 million dollars a day in potential revenue once plants reach capacity.

The Scale of What Is Coming

When Huayou's sulphate plant, Sinomine's Bikita expansion, and Yahua's Kamativi facility reach operational capacity, Zimbabwe's annual lithium revenue rises from 500 million to between 2 and 3 billion dollars. Treasury's fiscal capture doubles to 300 to 500 million annually.

If hydroxide and carbonate plants follow by 2029, revenue approaches 4 billion. If cathode precursor manufacturing arrives by 2030, enabled by the dual-track strategy, Zimbabwe's lithium value chain could generate 5 to 8 billion dollars a year.

At 8 billion, lithium alone would exceed the current value of all other Zimbabwean minerals combined. Gold, platinum, chrome, diamonds, nickel. All of them together. Smaller than lithium.

The African Development Bank projects over 1 billion dollars in annual lithium economic contribution within five years. The ISS African Futures initiative modelled the beneficiation policy and concluded it could add 2.4 to 3.1 percent to GDP growth if processing reaches planned capacity.

Let me make this personal. Because numbers in the billions sound like government talk until you translate them into the life you actually live.

Zimbabwe's formal economy is roughly 30 billion dollars. If lithium adds 3 billion in revenue at the sulphate stage alone, that is a 10 percent expansion of the national economic base within 24 to 36 months. Not a decade. Not a generation. Three years. If you own commercial property in Harare, your rental yields are denominated in an economy that just grew by a tenth. If you run a logistics company, there are processing plants in Goromonzi, Bikita, Kamativi, Mberengwa, and Buhera that need chemicals trucked in and product trucked out every single day. If you manufacture anything, the downstream procurement chain from a lithium sulphate facility needs packaging, water treatment, PPE, electrical components, civil engineering, and catering for a workforce that did not exist two years ago. If you are in financial services, the miners, the joint ventures, and the Chinese operators need treasury management, insurance, payroll, and foreign exchange facilities routed through Zimbabwean banks.

At the cathode stage, add another 5 to 8 billion. That is a 25 percent expansion. The person who owns five properties in that economy now holds the equivalent value of six or seven. The business generating a million dollars in revenue is operating in a market where aggregate demand has expanded by a quarter. Your net worth does not need to be directly connected to a lithium mine. It needs to be inside the economy that lithium is about to inflate.

The timeline is not speculative. Huayou's sulphate plant is commissioning now. Yahua broke ground in February. Sinomine's expansion is underway. The revenue hits Zimbabwe's economy the moment processed lithium chemicals leave the port at Beira. The first material shipments are expected before the end of 2026. The full revenue impact lands in 2027 and 2028. That is not the distant future. That is the next budget cycle.

Return to the question posed at the opening. Whatever you are worth today exists inside an economy shaped by 7 billion in mining revenue. Lithium is about to add 2 to 8 billion to that base over the next five years. The property you hold, the business you run, the contracts you service, the currency you save in, all of it sits inside a container that is about to expand by 30 to 100 percent. The people who position themselves inside the lithium economy before that expansion completes will be the wealthiest generation of Zimbabwean business operators since independence.

The Presidential Record

Consider what this means for the man who set it in motion.

When Emmerson Mnangagwa took office in November 2017, Zimbabwe's lithium production was negligible. The country was not ranked among global producers. Arcadia was an exploration-stage project owned by a small Australian junior. Bikita was a legacy mine producing modest quantities of petalite for ceramics. Sandawana was dormant. No Chinese processing investment existed on Zimbabwean soil. The word lithium did not appear in a single national budget document.

Eight years later, Zimbabwe is the fourth-largest lithium producer on earth. It holds the largest reserves in Africa. Over 1.4 billion dollars in processing investment has been committed. Three sulphate plants are under construction or commissioning. The Mutapa Investment Fund has been restructured into an operational mineral processing vehicle. A fiscal architecture that international mining consultancies describe as among the most sophisticated in Africa has been designed and implemented. The export ban has been executed at the precise moment of maximum leverage, when lithium prices are rising and processing infrastructure is ready to absorb domestic supply.

No Zimbabwean president has delivered a new billion-dollar export industry from inception to production in a single tenure. Ian Smith ran an economy under sanctions that never diversified beyond tobacco and chrome. Mugabe presided over the Marange diamond fields, a resource windfall that generated an estimated 15 billion dollars in rough stones. The country built no cutting facility. No polishing house. No jewellery manufacturing base. The diamonds left Zimbabwe raw, and the benefit left with them.

Mnangagwa's lithium trajectory is structurally different. The export ban ensures processing happens domestically. The Build-Operate-Transfer model ensures infrastructure transfers to state ownership. The fiscal gradient ensures Treasury captures an increasing share as value addition deepens. If even the first stage of chemical processing reaches capacity by 2028, the final year of the current presidential term, Zimbabwe will have added a 2 to 3 billion dollar annual revenue stream that did not exist when Mnangagwa took power. That is a legacy measurable not in speeches but in foreign exchange receipts, in processing plants visible from satellite imagery, in jobs that require chemical engineering degrees rather than pickaxes.

By 2030, if the dual-track strategy opens Western investment and cathode manufacturing arrives, the lithium sector alone could be generating more annual revenue than Zimbabwe's entire mining industry produced in 2017. The president who inherited an economy in crisis would leave behind an industrial asset base that fundamentally altered the country's position in the global supply chain of the twenty-first century's most strategic commodity.

Botswana's Seretse Khama is remembered for diamonds. Indonesia's Jokowi is remembered for nickel. Rwanda's Kagame is remembered for services and technology. The question of whether Mnangagwa will be remembered for lithium depends on whether the processing plants commission on schedule, the electricity constraint is resolved, and the next phase of investment is secured before the competitive window closes. The geology and the policy are his legacy. The execution is his test. And the scoreboard, unlike politics, does not lie. It is denominated in tonnes of lithium sulphate leaving Beira with a Zimbabwean certificate of origin.

The geology is confirmed. The fiscal architecture is in place. The processing capital is committed. The geopolitical demand is structural and growing. The competitive window is open but narrowing as Mali, the DRC, and Nigeria scale up.

The multiplication is seventy-two. Zimbabwe's current capture is five percent. The policy is designed to quadruple that within three years. The question for every decision-maker reading this is simple.

Where do you intend to be when the rock becomes the battery?

Until next time, Head Bowed.